The Fed v The Market (I’m betting on the Fed)

The Fed v The Market (I’m betting on the Fed)

From The Maven Letter: August 10, 2022

Stocks have been on a run. The S&P 500 is up 14% from its June low; the NASDAQ 100 is up about 20%.

Yet sentiment is dismal. Google searches for ‘recession’ are through the roof. The yield curve is more inverted than it’s been for 20 years, even after improving a bit today. And Fed officials keep reinforcing their message that they are nowhere close to finished hiking, stock market rallies be damned.

So what’s going on?

Basically, the bond and stock markets are fighting the Fed: traders that expect a recession, and soon, will halt further rate hikes. Not by September (the next Fed meeting), but in the 3-6 months after that.

Ok…but why are people buying stocks ahead of a recession? Good question. For the possibility of a soft landing? Just the gains (and game) of a summer rally? Because stocks are supposed to perform when bond yields are falling, which is one of the things that happens when a recession is expected?

All of those are likely playing a role. But understanding what is happening is only partly helpful in understanding what’s next. Because There a re multiple inverse cause and things only get more complicated from here.

There are multiple inverse cause-and-effects in play. For instance, the Fed needs financial conditions to tighten broadly. That means it needs the bond market to play along: it needs yields to rise across the spectrum, making money more expensive. Instead, yields are falling. The Fed also needs liquidity to fall because liquidity is inflationary, but this summer market run has been creating liquidity instead of draining it. Two indices that track financial conditions - one by Bloomberg and another by Goldman Sachs - both agree that conditions have eased considerably in the last six weeks (a higher reading means conditions are looser).

And so we get to backwards cause-and-effect number one: falling bond yields (because traders expect a recession) and rising share prices within this interim rally are undoing the Fed’s efforts and could end up forcing the Fed to push harder on rates – the exact opposite of what Fed Fighting Traders are expecting.

With so many contrary forces in play, it’s hard to see the future. The inflation numbers for July, out today, both helped and didn’t. CPI was lower than expected, coming in at 8.5% year-over year, down from 9.1% in June and less than the 8.7% forecast. Core inflation, which strips out food and energy, came in at 5.9% year-over-year, the same as June and below the 6.1% expected.

Has inflation peaked? It quite likely has. When inflation rises strongly its peaks don’t usually last long, because it to some extent fixes itself (people step back on buying as their purchasing power erodes) and because tightening adds downward pressure. That describes today…but it reveals nothing about how quickly and far inflation will fall.

If we could only know that inflation would drop sharply now that it’s peaked, it would be so much easier to know what to do next. But there’s no certainty on that. Yes, central banks are tightening. Yes, there’s regular talk that a recession is nigh, or perhaps that we’re already in one…but it sure doesn’t feel that way.

There are Help Wanted signs everywhere, airports are jammed, earnings are down but far from out as retailers have successfully passed cost pressures on to consumers, and stores remain full. Then there’s that stock market rally.

But the key 2-10-year yield curve is very inverted, which reliably predicts a recession. And the Fed promises to keep raising rates until inflation is tamed, even if that means pushing the economy into recession. So it’s coming, right?

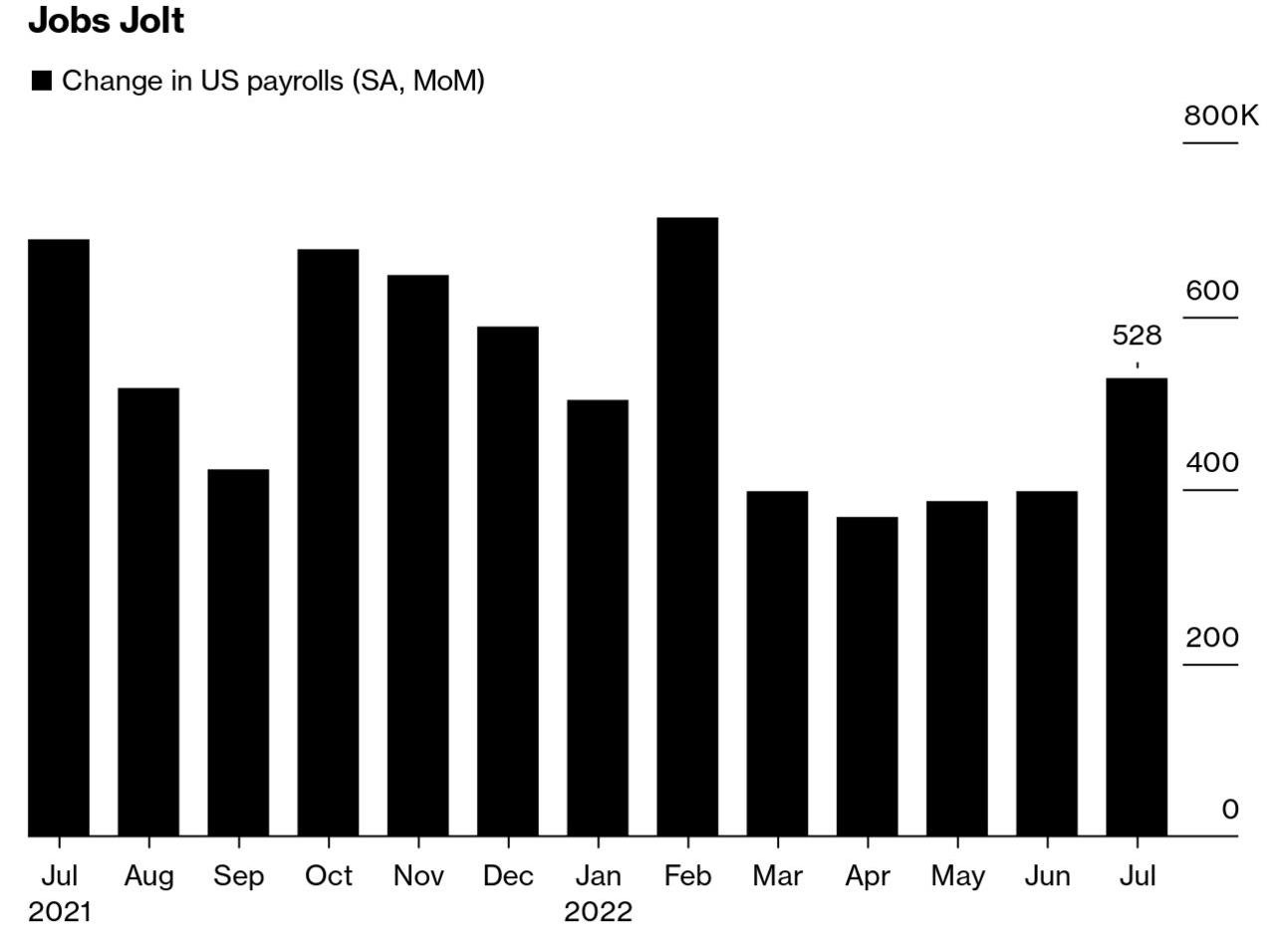

I think a big factor in recession complacency is the robust job market, because that is undeniably a huge recession cushion. If people can keep their jobs or get new jobs if needed, the situation will remain way better than if they can’t remain employed. The chart below, out following July’s strong US jobs report, doesn’t shout ‘recession!’

And labour tightness is forcing companies to increase wages, perhaps not in lockstep with inflation but reasonably, which supports ongoing spending.

But…it’s generally accepted that there’s a 3 to 18-month lag between a central bank hiking rates and those rate hikes having economic impact, with tightness usually starting to hit 6 to 12 months after the first hike. In a few days it will be 5 months since the first hike of this cycle…which means we have barely begun to feel the impact.

But impacts will come. Take a moment to remember that the Fed spiked short-term interest rates from zero to 2.25% in just four months. The drama of that move created a lot of fear and that fear pulled markets down in the spring…but with tightening still not really hitting yet, stocks were able to rally through the summer.

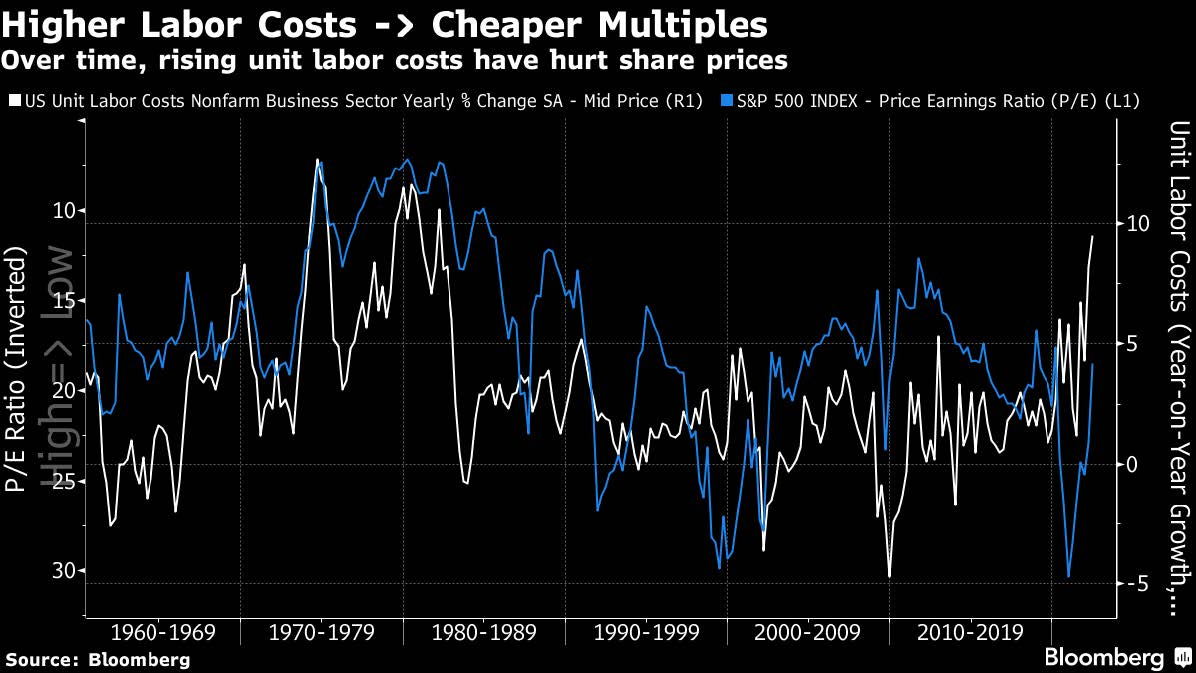

What will tightening do when it truly hits? I’ve noted often that the best correlation for stocks is earnings. As interest rates rise and debt service costs increase and inflation juices spending, earnings fall. We saw unit labour costs make their biggest year-on-year rise since 1982 in the second quarter. Higher wage pressures plus productivity challenges will do that.

There is a strong inverse correlation between unit labour costs and earnings multiples – if labour costs are rising, you should expect multiples to drop. (Earnings multiples are shown inverted in blue below.)

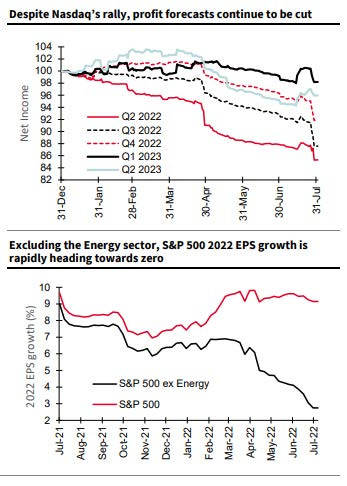

This is all happening but the process of downgrading forward earning estimates is only just beginning: as the charts below from Societe Generale’s chief strategist Andrew Lapthorne show, Nasdaq profit forecasts for the next four quarters have been cut. And the buoyancy of the energy sector hides the fact that, for the rest of the S&P 500, the earnings growth forecast for this year is close to nil. Those trends say stocks are set to slide.

Why isn’t the stock market dropping then? For now, because companies have been able to pass costs on to consumers, thus preserving profit margins. How long this can last is a big question.

Then there’s liquidity. Economic growth and increased investing come down to how much money is available within corporations and households. One great gauge of real liquidity – readily available money minus what is being used for economic output – continues to decline, pointing to a sharp economic slowdown over the coming months at best.

At the end of the day, I just don’t think inflation will slip gently away. And data from the new CPI report backs me up.

Certain prices that were directly affected by the pandemic are absolutely easing. Prices for used cars, car rentals, and airfares, for instance, spiked dramatically in 2021 and are now coming back to earth.

That’s great…but the Fed never cared that much about these prices. Instead, the Fed cares about sticky prices, the inflation rate for which according to the Atlanta Fed’s sticky CPI measure just high a 40-year high. Then there’s housing, which makes up about a third of the CPI index; year-on-year inflation in owner-equivalent rent rose again last month to set a new high since 1990.

In short: there are oodles of reasons to believe the Fed has a LOT of tightening left to give. And the only line of reasoning behind a rising stock market is the belief that the Fed will pivot to easing sooner rather than later.

I just don’t think that line of reasoning will stand up for the next six months. Let’s be very clear: 8.5% inflation is an improvement on 9.1% but it’s still far from an acceptable rate. The Fed does not want to make the mistake of the early 1970s when they reversed tightening at the first sign of an economic slowdown, which allowed inflation to get entrenched. So they will keep raising rates.

Inflation might have peaked. The questions from here are:

How much will inflation come down now that commodity prices (energy and metals) are normalizing and supply chains are healing? Will those helps bring it to…6%? 5%? Against that, what rate of inflation is acceptable? It takes a lot more time and much tighter conditions to contain sticky prices like rents than flexible prices like gas or food.

Where is the jobs market really heading? A tight jobs market will keep inflation

pressures high – employers will pay to retain workers, which adds liquidity to the system and supports ongoing price growth.

What will the stock market care about? Earnings? Interest rate moves? Inflation

numbers? Yield curves? It certainly feels like there’s still more than enough liquidity out there to fuel moves from traders wanting to play the moment, which is a force that dwindles considerably in a real recession. Several meme stocks, including bankrupt AMC, jumped last week for this exact reason (not for any good reason, let me be clear).

I can identify the questions. I don’t have the answers.

I think there’s still downside ahead. I think the market – traders – are getting ahead of themselves in their optimism that the Fed will pivot anytime soon. Like I said, 8.5% is still a totally unacceptable rate of inflation. It’s 13% in England, where the central bank just enacted a 50-basis point hike while pointing to an impending recession.

Those are big numbers. It will take significant tightening to rein them in. The way stocks have run of late, traders are either very complacent about the tightening to come (they still think the Fed will prioritize the stock market over its inflation mandate?!) or they are simply taking a lot of advantage of an interim opportunity.

Because this is an interim moment. There is more tightening to come. Powell and co don’t care about your portfolio; they care about inflation and they will tighten until it is well down. That amount of tightening will hurt – it always does and might especially this time given corporate debt loads.

It’s been a weird tightening cycle so far. Everyone expects a recession but I just don’t know what that recession will look like in terms of jobs and costs and earnings, and so I don’t know what it will mean for liquidity and stocks.

And that’s where the rubber meets the road for metals investors, because:

No one buys growth when times are tough, so base metals are out of favour until the idea of recovery comes into the conversation (fundamental supply gaps within a few short years, like for copper, be damned)

No one really leans into gold until the worst is over, or at least underway. Gold slides along with everything else in a recession. It doesn’t protect against downside – but it does recover first. So gold also requires the worst to be underway.

I wish I were more optimistic than all this…but I just can’t ignore the realities ahead.

That said, after several months avoiding companies that wanted to meet (because I didn’t want to get pitched when I was not interested in buying anything), I am now back to taking meetings. And I’m planning my trip to the Beaver Creek conference next month, which brings together institutional investors (and folks like me) with junior and mid-tier resource companies for one-on-one meetings.

I’m still very hesitant on buying anything. But because it turns first I think gold could bottom by the end of the year, which isn’t all that long from now. And the fundamental arguments behind copper, lithium, uranium, silver, and nickel are insanely strong; those opportunities will surface over the next 6 to 12 months and one should never wait until the opportunity is here to prepare. And really good teams use weak market moments (months, years – whatever the case) to establish new ventures or push projects ahead, so I want to hear about what people have been doing.

I also was reminded that the market will reward really good discoveries no matter what is going on. For evidence, look no further than Snowline Gold (while looking at the share price chart, imagine me hitting my head against a wall…):

Yes, I have known about this company for the last year. Yes, I have met with them. Yes, I thought their projects looked very promising. Yes, the company itself met all the other requirements I make of junior explorers.

No, I did not invest, because the macro setup held me back.

Yes, it’s a poignant reminder that discoveries matter through thick and thin.

I am meeting with Snowline for an update on Monday. My goal is to understand what the opportunity looks like from here. I’ll let you know…

This content is available thanks to subscriber support. To subscribe to the full newsletter, see subscription options here or click the button above.

Add the RESOURCEMAVEN30 promotional code at checkout and get 30% OFF!